Background

I wanted to learn about finance, so I started to take some courses in it. It’s been nearly a year, and I have learned a ton. To help reinforce what I’ve learned (and to share the knowledge), I plan to write about finance every once in a while. For this first article on finance, I wanted to write about the Markowitz portfolio variance.

In finance, one of the most important discoveries was by Harry Markowitz when he figured out how to measure the portfolio variance. It is used in modern portfolio theory to estimate the combination of investments that would reduce idiosyncratic risk, which is inherit in the asset (or a group of assets). Idiosyncratic risk is unrelated to the risk in the market. Rather, it is the risks when assets that you invest in are correlated with each other. The more correlated they are, the more risky they become.

Assets that are part of the same sector or type tend to be correlated with each other. For instance, General Motors is an automobile company, and its stock price will likely be correlated with another automobile company like Ford Motors. If you want to diversify your portfolio, investing in both General Motors and Ford Motors increases your idiosyncratic risk since both investments would be part of the same sector. If one of these firms does poorly, it is likely that the other firm will do poorly.

Markowitz was able to develop an equation that would capture the idiosyncratic risk associated with a combination of assets in an investment. His portfolio management variance calculation uses the standard deviation of one asset (Asset A) and its correlation with another asset (Asset B). In other words, Markowitz’s formula incorporates the correlation between assets. By incorporating the correlation between assets, an investor can estimate the idiosyncratic risk of their investment strategy and avoid stocks in market sectors that would potentially be a greater risk due to their correlation.

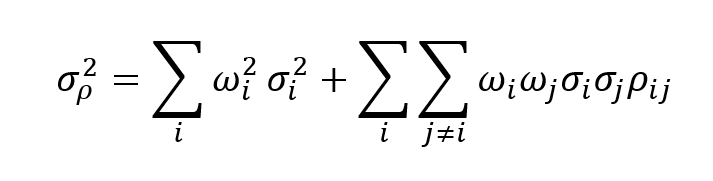

Markowitz’s portfolio variance formula for a combination of two assets (i and j) is structured as:

where:

sigma_p^2 is the portfolio variance

w_i is the weight of Asset i

w_j is the weight of Asset j

sigma_i^2 is the variance of Asset i

sigma_j^2 is the variance of Asset j

rho_{i, j} is the correlation between Assets i and j

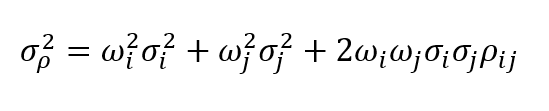

We can simplify this expression for a two-asset portfolio as:

Motivating Example

Let’s look at an example. Suppose we have two assets (i and j) that we want to diversify our portfolio with. We’re concerned about the idiosyncratic risk between the two. We can use this formula to estimate the idiosyncratic risk. (Note: You can download the Excel exercise from my GitHub repository here.)

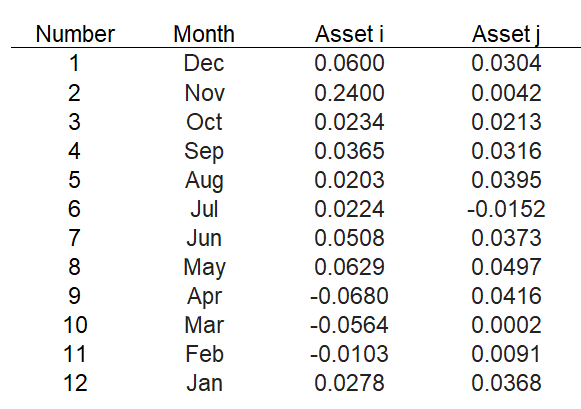

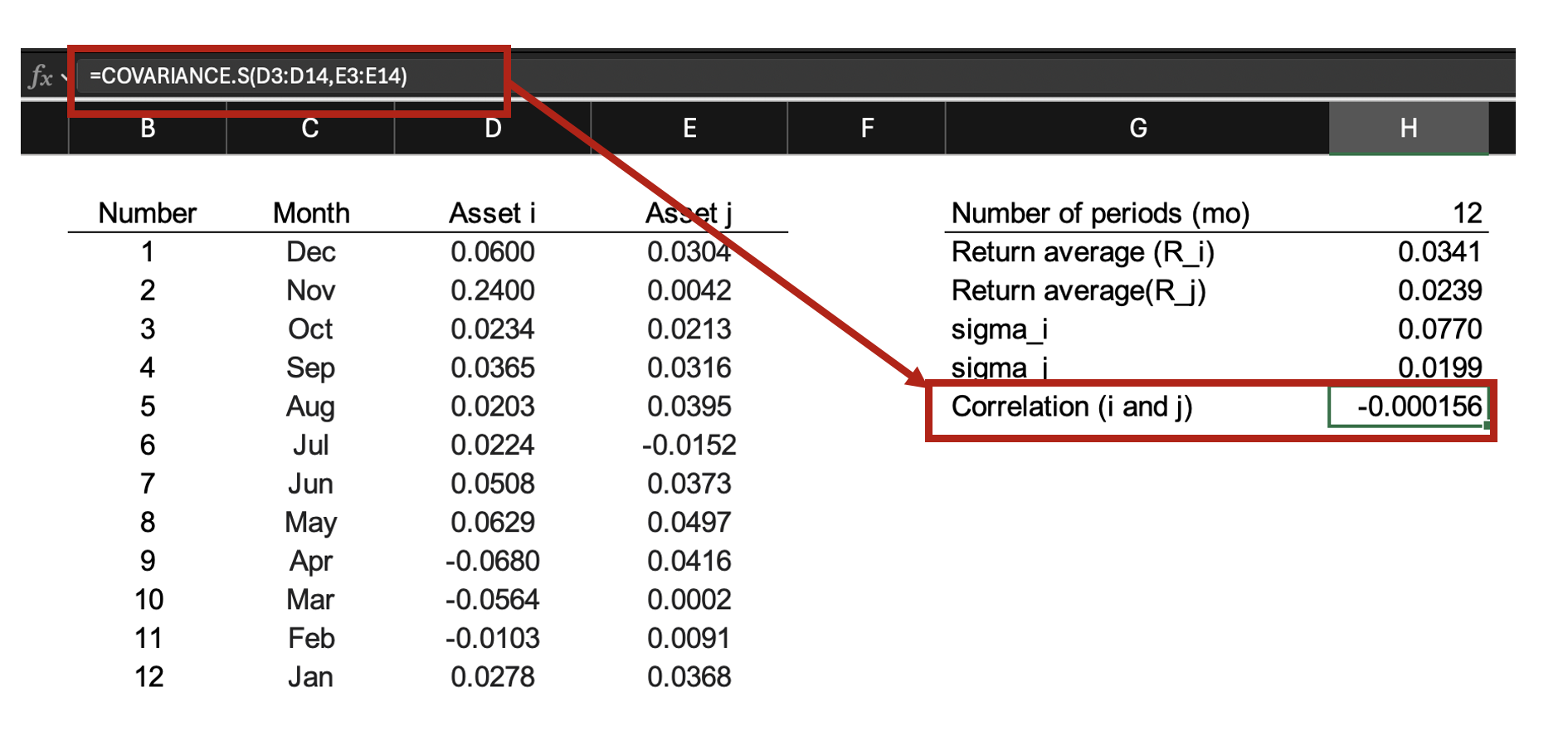

Here is the data for the returns for Assets i and j:

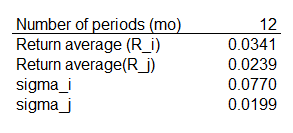

We can estimate the average returns for Assets i and j along with their standard deviations.

Then, we can estimate the covariance between the two assets’ returns.

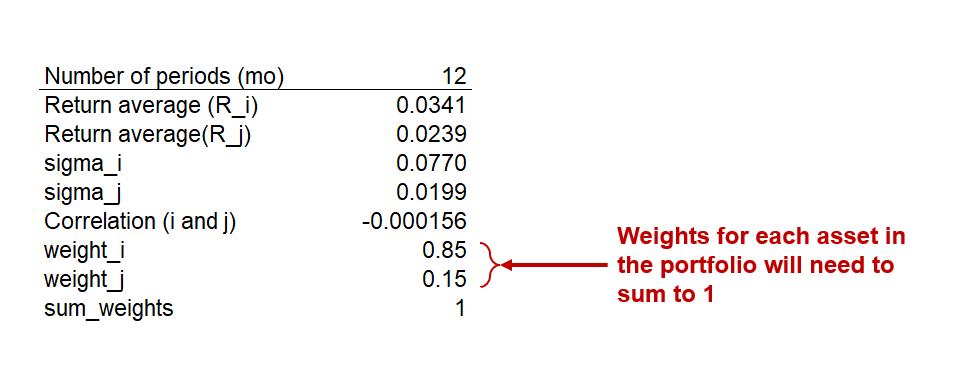

Next, we need to apply weights to the assets. Let’s assume that we want to place more weight to Asset i compared to Asset j. The weight for Asset i will be 0.85; hence, the weight for Asset j is 0.15 (or 1 – 0.85). The sum of the asset weights need to be 1.

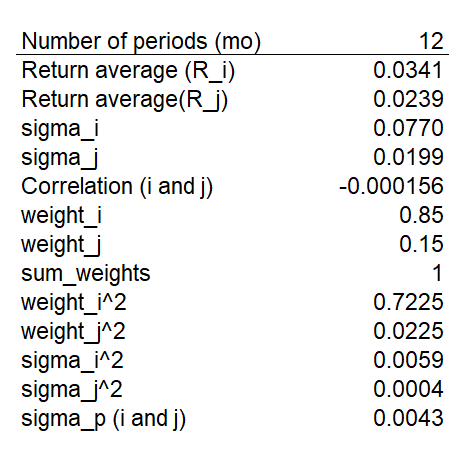

Once we have estimated all the parameters, we can now combine them using the Markowitz portfolio variance formula.

The idiosyncratic risk is 0.0043, which is pretty low since the correlation between Asset i and Asset j is very small (rho = -0.000156).

Concluding thoughts

There is more to modern portfolio management, but this is just the first part. As we continue in future lessons, we will build upon this knowledge by learning about how we can use the Markowitz portfolio variance to determine the risk and return tradeoffs.

Disclosure and Disclaimer

Since this is a work in progress, expect updates in the future.

Meanwhile, this is for educational purposes only

References

You can learn more about Harry Markowitz on Wikipedia here.

You can also learn more about portfolio variance on Investopedia here.

You can download the Excel exercise from my GitHub repository here.